Your existing TCFD (Task Force on Climate-related Financial Disclosures) reporting will not satisfy UK SRS S2 (UK Sustainability Reporting Standard S2). The gap is not structural: the four pillars of governance, strategy, risk management and metrics carry over directly. The gap is about evidence. UK SRS S2 requires you to quantify the financial effects of climate risks at asset and value-chain level, where TCFD lets you describe them. For most listed companies, producing that evidence to investor and auditor standard takes 12 to 18 months, which makes now the right moment to assess where you actually stand.

How does UK SRS S2 differ from TCFD?

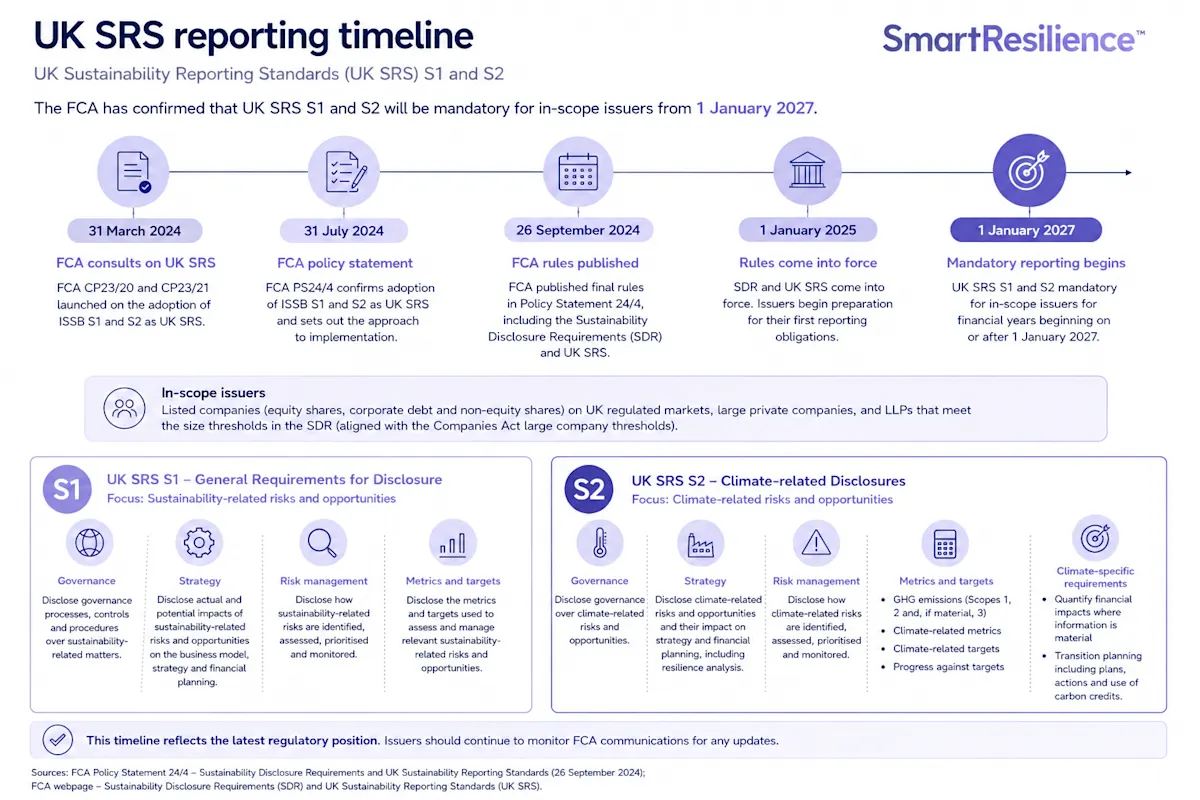

UK SRS S2 uses the same four-pillar structure as TCFD but demands a materially higher standard of evidence on physical risk, financial effects and supply chain coverage. The UK government published UK SRS S1 and S2 on 25 February 2026 as the UK's implementation of the ISSB's (International Sustainability Standards Board) IFRS S1 and S2. The FCA's (Financial Conduct Authority) January 2026 consultation paper CP26/5 then set out proposals to make UK SRS S2 mandatory for in-scope listed companies for reporting periods from 1 January 2027. For a full breakdown of the existing TCFD disclosurerequirements these proposals replace, see our related article.

The practical differences sit across five dimensions:

Dimension | TCFD | UK SRS S2 |

Scenario analysis | Qualitative narrative; two or more scenarios including a well-below-2°C pathway recommended | Quantified financial effects required where feasible; explicit explanation required where not provided |

Physical risk disclosure | Portfolio-level qualitative assessment of acute and chronic risks | Site-level and value-chain concentration disclosed by geography, facility and asset type |

Financial effects | Description of potential financial impacts on strategy | Current and anticipated effects on financial position, performance and cash flows, stated quantitatively where feasible |

Supply chain | Recommended to consider value-chain risks | Physical risk concentration across the full value chain disclosed from the first reporting period |

Assurance | No formal assurance requirement | ISSA (UK) 5000 applies for reporting periods beginning on or after 15 December 2026 |

The shift that matters most for most sustainability and compliance teams is the move from description to quantification. TCFD lets you frame physical risks qualitatively. UK SRS S2 requires you to state where they concentrate, in what financial terms, and why you excluded anything you could not quantify.

Who has to comply with UK SRS S2 and by when?

Approximately 515 primary-listed UK companies must comply with UK SRS S2 for accounting periods beginning on or after 1 January 2027, under proposals set out in FCA CP26/5, covering companies listed under UKLR (UK Listing Rules) categories 6, 14, 15, 16 and 22. Companies outside that threshold still face significant commercial pressure: lenders and insurers are already asking for the same data independently of legislation, and the cost of not having it is showing up in refinancing conversations and insurance renewals. For context on how TCFD recommendations integrate into financial reporting, see our related article.

Scope 3 emissions disclosure sits on a comply-or-explain basis from 2028, giving companies more time to build supplier emissions data. That phasing does not apply to physical risk supply chain disclosure, which is in scope from day one. Large private companies and LLPs are not yet mandated, but the direction of travel is clear and boards are increasingly asking why preparation has not started.

Practical tip: Use the 2028 Scope 3 phasing strategically. Begin building supplier physical risk coverage now alongside your own-asset work, so that when Scope 3 becomes mandatory the data infrastructure is already in place rather than a separate project starting from scratch.

UK SRS S2 preparation and its applicability to global ISSB reporting obligations

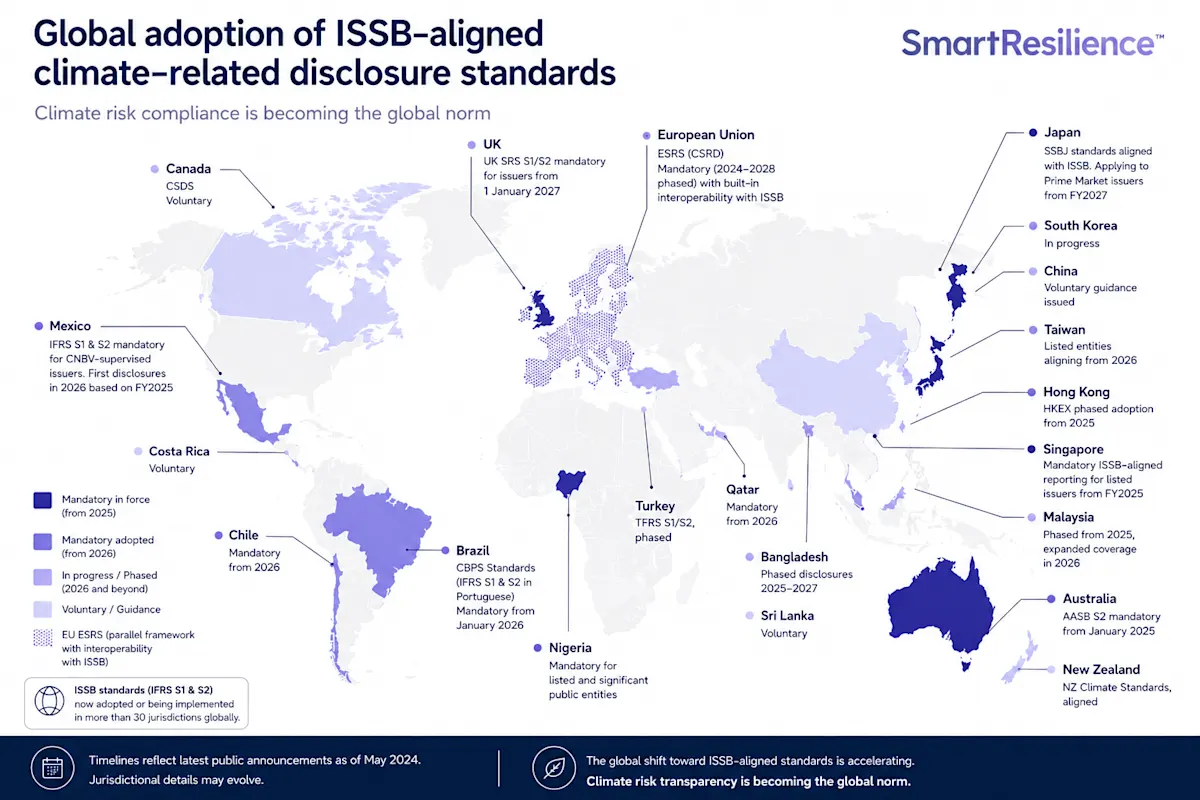

UK SRS S1 and S2 are the UK's implementation of the ISSB's IFRS S1 and S2, which means the evidence base you build for FY2027 is already the evidence base every other ISSB-aligned jurisdiction requires. The IFRS Foundation reports that 36 jurisdictions have adopted or are taking formal steps to introduce the ISSB Standards, with 21 having adopted them on a voluntary or mandatory basis as of 1 January 2026.

For multinational groups, this convergence is a practical advantage. Rather than running parallel climate risk workstreams for each jurisdiction your group reports into, you build one ISSB-aligned evidence base - site-level physical risk modelling, financially expressed, with full audit lineage - and map it to local rules. The EU's ESRS framework has interoperability with ISSB built in, so the same outputs cover both. The cost saving is material, and a single governed evidence base is substantially easier to assure than separate jurisdiction-by-jurisdiction models.

Does my existing TCFD scenario analysis meet the UK SRS S2 standard?

For most listed companies, no - and the reason sits in the output format, not the underlying methodology. Only 4% of companies were fully aligned with all 11 TCFD recommendations by 2023, according to the TCFD 2023 Status Report, with scenario analysis consistently identified as the weakest area. UK SRS S2 raises the bar above where most organisations currently sit.

A typical TCFD physical risk disclosure contains a portfolio-level heat map showing exposure by hazard type, qualitative materiality statements and generic references to RCP (Representative Concentration Pathway) or SSP (Shared Socioeconomic Pathway) scenarios. That satisfied TCFD. Under UK SRS S2, companies must disclose the current and anticipated financial effects of physical climate risks on their business model, financial position and cash flows, and demonstrate how risks concentrate by geography, facility and asset type. Where quantification is feasible it must be provided. Where it is not, the company must explain why, and auditors, regulators and investors will see plainly which companies can measure climate risk and which cannot. For a detailed look at how data quality gaps undermine CSRD and TCFD compliance, see our related article.

“Most of the TCFD disclosures we review are well-structured and credibly written. The problem is the underlying evidence. When we map them against UK SRS S2, the gap is not in the narrative, it is in the numbers. Companies have described their climate risks clearly. They have not priced them.”

— Edward Packshaw, SmartResilience

The investor environment has already shifted. Analysts and lenders have started tracking quantified climate exposure across portfolios, and companies filing narrative-style disclosures are increasingly being asked to explain what they cannot measure. UK SRS S2 formalises a standard the market was already moving toward.

Use this checklist to assess your current position:

Site-level outputs: Do your physical risk scenarios produce site-level results rather than portfolio aggregates?

Financial expression: Can you state physical risk exposure as expected annual loss or event-loss at specific return periods?

Value-chain coverage: Do your outputs cover supplier locations and logistics nodes as well as your own sites?

Revenue linkage: Do you have a traceable line from hazard data to revenue impact by product, market or customer segment?

Audit lineage: Can your scenario analysis be explained to an external auditor with full data lineage and methodology documentation?

Finance sign-off: Have your finance and risk teams reviewed and agreed the financial assumptions underpinning your climate scenarios?

Most teams find their current outputs answer yes to one or two items and need significant development across the rest.

Key takeaway: The transition from TCFD to UK SRS S2 is a capability gap, not a documentation gap. Updating a report structure does not close it. Producing site-level, financially expressed physical risk evidence does.

SmartResilience

See SmartResilience in action

Book a free demo tailored to your organisation and assets.

Book a free demoWhat does UK SRS S2 require on supply chain climate risk?

UK SRS S2 requires companies to disclose where physical climate risks concentrate across the full value chain, including supplier locations and logistics nodes, not just owned assets. Supply chain physical risk disclosure applies from the first reporting period under the standard; it is not deferred alongside Scope 3 emissions. Scope 3 sits on comply-or-explain until 2028, but the physical risk concentration requirement has no equivalent relief. For more on supply chain transparency under CSRD, including how to gather and report supplier data, see our related article.

In practical terms, a flooded supplier facility in a coastal industrial zone, a heat-disrupted port creating a logistics bottleneck, or a drought-constrained agricultural input affecting product availability are all disclosable physical risks under UK SRS S2. Each requires the same quantification standard as own-asset exposure: where it sits in the value chain, what the financial effect could be, and what the company is doing to manage it.

The starting point is geocoding critical supplier locations and logistics nodes against multi-hazard climate models, then running expected-loss analysis across the same scenarios applied to owned assets. For most companies this means building a supply-chain risk data infrastructure from scratch, which adds directly to the 12 to 18 month evidence-building timeline. This is where the timeline becomes concrete for most teams.

What does UK SRS S2 mean for my transition plan?

UK SRS S2 expects companies to disclose information about any climate-related transition plan, including the assumptions used and how it will be resourced. A transition plan that cannot be backed by quantified physical risk evidence will not hold up to investor or auditor scrutiny under the new standard.

To stand up, a transition plan needs to show, at minimum:

Risk location: Where physical and transition risks sit across the asset base and value chain, by site and geography

Risk evolution: How those risks change under different scenarios and time horizons, expressed in financial terms

Loss quantification: What risks could cost in expected annual loss and tail-loss terms across return periods

Adaptation evidence: Which adaptation and mitigation actions reduce that loss, modelled by ROI

Investment profile: The capex and opex required to deliver those actions, costed and sequenced

Quantification is the spine of all of this. Without site-level physical risk modelling, financially expressed, a transition plan is a narrative document. Under UK SRS S2, narrative without numbers will be flagged by auditors reviewing the evidence base, by investors asking how the plan is resourced, and by regulators assessing whether disclosures meet the standard's requirements on financial effects.

How long does building UK SRS S2-ready evidence actually take?

Twelve to 18 months is the realistic timeline for physical risk evidence that holds up to investor and auditor scrutiny under UK SRS S2. Geocoding sites against a hazard model is step one of approximately ten. The work that takes the most time is translating physical hazard outputs into revenue impact by product, market and customer segment; modelling business interruption losses across own operations and critical supply chain nodes; agreeing P&L and cash-flow sensitivities with finance; and building adaptation and resilience actions with costs, sequencing and ownership documented.

That cross-functional alignment requires sustainability, risk, finance, operations and procurement to work from a single set of numbers. It cannot be compressed into a quarter, and it cannot be completed in the run-up to a year-end filing.

The assurance dimension adds further urgency. ISSA (UK) 5000, the sustainability assurance standard, applies for reporting periods beginning on or after 15 December 2026. The evidence base must be defensible before it reaches the assurance provider, not after. Auditors reviewing physical risk disclosures under UK SRS S2 will distinguish between organisations that have built a robust, governed evidence base and those that have attached numbers to a narrative. Companies targeting credible FY2027 disclosure are putting those foundations in place now.

What does UK SRS S2-ready physical risk evidence look like in practice?

UK SRS S2-ready physical risk evidence quantifies exposure at site level, expressed as expected annual loss and event-loss across return periods, with full audit lineage traceable back to the underlying hazard data. £3m of flood exposure quantified across 1,000+ Sainsbury’s sites illustrates exactly what that looks like: physical risk mapped by geography and facility, expressed in financial terms, with methodology an auditor can follow.

Working with SmartResilience, your sustainability, risk and finance teams produce:

Site-level climate scenario modelling through 2100

Expected annual average loss figures by site and hazard

Event-loss views across return periods from 1-in-20 to 1-in-1000 years

Supply-chain physical risk covering supplier locations and logistics nodes alongside owned assets

Those outputs feed directly into the financial effects disclosures UK SRS S2 requires. The same evidence base covers every other ISSB-aligned jurisdiction your group reports into, so the work done for the FCA does not need to be replicated for other regulators.

SmartResilience works alongside your internal teams as a continuously updated system rather than a one-off modelling exercise. The evidence base built for FY2027 stays current as your portfolio evolves, as regulations develop and as climate projections are updated.

Frequently asked questions

How is UK SRS S2 different from TCFD?

UK SRS S2 uses the same four-pillar structure but requires financially quantified physical risk at site and value-chain level. TCFD accepted qualitative scenario narratives. UK SRS S2 does not, unless a company can demonstrate why quantification is not feasible.

Who has to comply with UK SRS S2?

Approximately 515 primary-listed UK companies, covering UKLR categories 6, 14, 15, 16 and 22, for accounting periods beginning on or after 1 January 2027, under proposals set out in FCA CP26/5.

What does “quantify the financial effects of climate risk” mean in practice?

It means expressing physical risk exposure as expected annual loss or event-loss across return periods, at site level, by geography and hazard type, with a traceable line to revenue impact and financial position, not a qualitative description of potential impacts.

Does my existing TCFD scenario analysis meet UK SRS S2?

For most companies, no. The gap is the output format: TCFD accepted portfolio-level qualitative narratives. UK SRS S2 requires site-level, financially expressed evidence. Only 4% of companies were fully aligned with all 11 TCFD recommendations by 2023, with scenario analysis the weakest area.

What does UK SRS S2 require on supply chain climate risk?

Companies must disclose where physical climate risks concentrate across the full value chain, including supplier locations and logistics nodes, from the first reporting period. This applies regardless of the Scope 3 comply-or-explain phasing, which covers emissions only, not physical risk.

How long does it take to build UK SRS S2-ready physical risk evidence?

Twelve to 18 months for evidence that holds up to investor and auditor scrutiny. Hazard mapping is the starting point; translating outputs into site-level revenue impact, agreeing financial assumptions with finance, and building adaptation actions with costs and ownership is where the time is spent.

What is the difference between UK SRS S2 and IFRS S2?

UK SRS S2 is the UK’s implementation of IFRS S2, published 25 February 2026. The standards are closely aligned. Multinationals reporting under both can build one evidence base and map outputs to each standard, avoiding parallel workstreams.

What happens if I file narrative-style disclosures under UK SRS S2?

Companies must explain why quantification was not provided. Auditors, investors and regulators will see which companies can measure climate risk and which cannot. As investor expectations have already shifted toward quantified evidence, narrative-only disclosures carry increasing scrutiny risk.

Should I wait for the FCA’s final rules before starting?

Waiting for the FCA’s final rules before beginning the evidence-building process means losing the 12 to 18 months the process actually requires. By the time rules are confirmed, the available preparation time no longer supports credible quantitative disclosure for FY2027. Companies that wait will be the ones filing narrative-style disclosures into an investor environment that has already stopped accepting them.

For teams evaluating which platforms can support this work, our review of Climate Risk Management Software Compared: 6 Platforms Reviewed for 2026 covers the key options against UK SRS S2 readiness criteria. The companies filing credible disclosures in 2028 are starting the underlying work now.

Book a SmartResilience UK SRS S2 readiness assessment. In one session, our team maps your existing TCFD outputs against UK SRS S2 requirements, identifies where the quantitative evidence gaps sit, and shows you what site-level and supply-chain physical risk disclosure looks like in practice.